I had one of my weekly “duh” moments Wednesday.

A just-released study from the LIMRA Secure Retirement Institute found that half of all U.S. households of pre-retired and retired people who have at least $100,000 in assets are interested in converting those assets into guaranteed lifetime income.

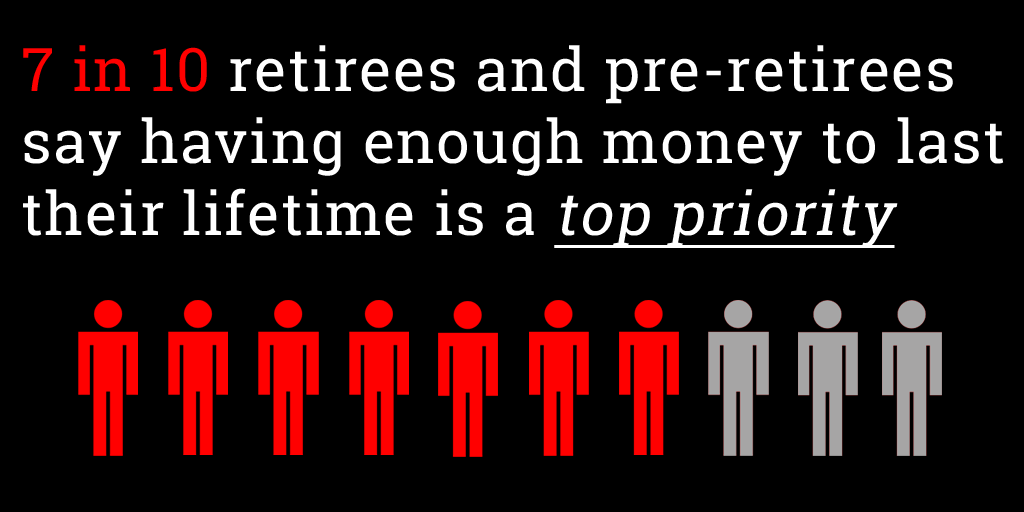

“Our research shows that these demographic segments are less likely to have a defined benefit pension plan and will have to rely on their own assets to create retirement income,” said a spokesman for LIMRA. “Our study found 7 in 10 retirees and pre-retirees say having enough money to last their lifetime is a top priority, and nearly two-thirds want to remain financially independent in retirement.”

The 50-59 age group was most interested in converting assets to guaranteed lifetime income at 55%, followed closely by those who were not yet retired at 54 percent, and those with household assets between $100,000 and $499,000.

And, why not? Most of them got whacked upside the head in 2008 and, if they are lucky today, are back to where they were six years ago. Not only are they having to work longer, many of them (as the research found) have little appetite for risk in the markets.

Enter Indexed Universal Life (IUL).

You know I’m a big fan and the numbers above reinforce the huge market need. The big question, with the knowledge above, is why aren’t more agents presenting IUL to clients?

An IUL is simply an overfunded universal life policy that has guarantees to create a lifetime payout. Imagine being paid out of a life insurance policy while you’re still alive and then, when you die, there’s still a death benefit for your loved ones.

Clients with large IRAs are a great target. At some point taxes are going to chew up a big portion of an IRA. Opening an IUL account is a great alternative. The client can take tax-free distributions of the cash value when they retire by borrowing from the policy. And, when the client passes away the tax-free benefit protects their families. And, the client pays no taxes during the time they are contributing cash to the policy.

Because IULs are not directly tied to stock markets, the risks are minimal. And, the ratchet and reset feature locks in gains from the previous year so even if the market crashes there are no losses. If you haven’t taken a look at the impacts a max funded IUL can have on your clients portfolio, now is the time.

And, unlike an IRA, there are no limits on how much a client can contribute to an IUL.

The LIMRA research reinforces the market segments that would benefit from an IUL: those with large IRAs, high earners looking for more protection from taxes or simply someone looking for more ways to save tax free.

There’s a book by Patrick Kelly I like to give clients called “Tax Free Retirement”. It breaks down the options for clients into simple concepts. It’s a great book you should read and give to clients. Call or email me if you would like to discuss.

Product of the Week: EquiTrust MarketTwelve Bonus Index annuity

EquiTrust’s MarketTwelve Bonus Index annuity is one of the most competitive fixed annuities on the market today. This offers clients a product based on how it will perform, not how it might perform, due to its extremely competitive lifetime income rider. The MarketTwelve also offers long term care options for clients who want to make sure their assets are available in the event they are confined to a nursing home. These are just two of the great benefits of the MarketTwelve Bonus Index annuity. Below is a summary of what you can expect to offer your clients by carrying EquiTrust’s MarketTwelve Bonus Index in your product portfolio.

EquiTrust is a part of the Guggenheim Partners family and Guggenheim provides operational and portfolio management for EquiTrust Life. This allows EquiTrust to continually serve clients through a series of high quality retirement services.

- Issue Ages: 0-75

- 100% nursing home rider

- Lifetime income rider

- Qualified and non-qualified options

- Bypass probate

- 6% bonus year 1

- 2% compounded bonus year 2

- 2% compounded bonus year 3

- 2% compounded bonus year 4

- 12% TOTAL bonus!

- $30,000 minimum contribution

- Multiple crediting methods

- 60-day rate holds

Redbird Chirps

- Women more positive after getting financial advice. However, 66 percent struggle to find a resource they can trust in a recent LIMRA research study. Wow. And, more women are finding it hard to make time for this. Some interesting stuff in here. Read more.

- 9 ways to be a positive communicator. We can never hear these common sense words of advice too often. One we love that isn’t literally on the list (but it’s there in spirit): Smile when you’re on the phone. It works. Read more.

- Future: Get ready for clients who keep on living. This was a great read. This futurist has developed four scenarios for our future. Which one do you think will occur? Read more.